It’s a funny thing how certain concepts have permeated throughout our culture and are just simply accepted as ‘normal’ without question. Even when faced with the reality that a given ‘normal’ situation is in jeopardy or worse, may all together cease to exist, we as a society still measure and plan our lives based upon what we thought was supposed to happen. If we feel we are entitled to it, then not only do we cling to it, but we do so with anger and righteous indignation.

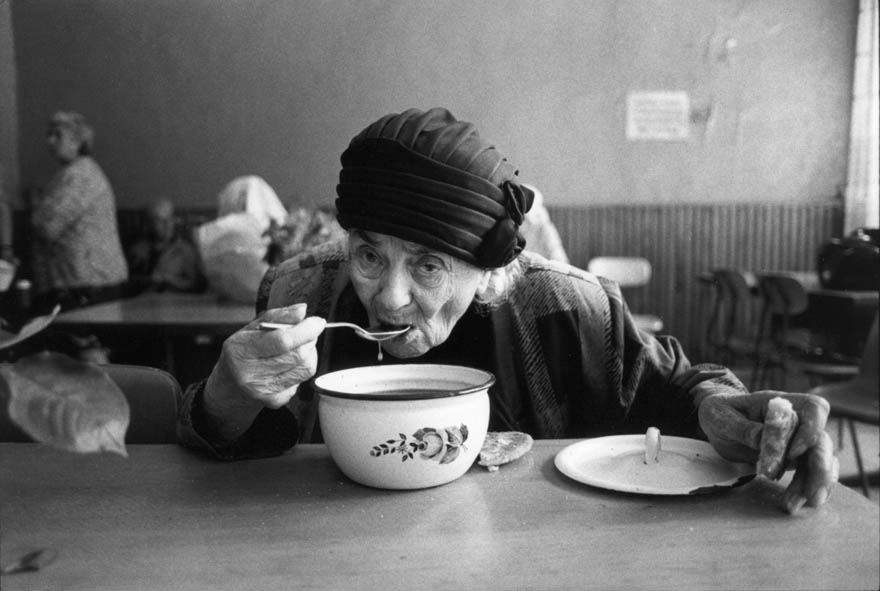

One of the most brilliant public relations campaigns launched in modern times is the concept of retirement. The idea of working hard all our lives while carefully saving and investing so that we may spend our twilight years financially independent while relaxing, playing and enjoying all the things life has to offer as a reward is romantic and hard to resist. The people who believe this is the norm will be the same ones who claim “I did everything right. I played by all the rules. It's not fair. I was robbed.”

To add insult to injury, those of us who will not benefit from this version of the bought and sold concept of retirement were a party to watching the generations before us experience precisely that. In the world’s greatest recorded wealth cycle and bubble of all ages, where the world eventually levered over a quadrillion dollars in bets, the wealth effect has been tremendous and many in the Western world were able to jump on for the ride. Overdue for the boom to go bust, the latter generations will not enjoy the picturesque golden years in style and comfort as sold to us in the retirement brochures.

Even as the more aware and savvy among us understand the wheels are coming off the economic bus presently on a worldwide centrally planned disaster tour, the continuity bias is astounding as I watch those with assets address this as an “extra rough patch” to get through rather than the clear paradigm shift it has been telegraphed to be. Further, even those who see what is now underway and acknowledge this as a game changer think they can game the system, escape the worst of it or hedge enough to have one of their winning bets fall somewhere solid.

No, it isn’t fair. But blaming the generations who prospered before us or the central planners and bankers who we enabled will not bring back that comfy old age experience we had hoped and planned for. As painful of a time as this will be, perhaps this is a good time to think about "if not retirement, then what”.

For a brief time it may appear that working a low wage job in a position perceived far beneath our qualifications is the only future the system has left for us. And it may very well be so if we still allow the same system that sold us on ‘retirement’ to define what we will do, or be, without it.

Perhaps it's time to give deep consideration to rethinking any concept that depends upon the way the system is supposed to work. Public and private pensions, social security and annuity payments will not be getting the job done. We fully expect IRA and Roth retirement investment vehicles will be largely forced to convert some or all holdings into U.S. Treasuries……for your own safety of course. Capital controls and changing the financial and social rules will become the new normal. Cash and any residual savings can simply be ‘bailed in’ to ‘bail out’ the big boys through the banks and brokerages that hold the funds.

Finally even if these retirement vehicles could be liquidated and placed in currency stacks before us, after we pay outrageous penalties and taxes of course, there is no sure way to preserve it. Certainly there are no ‘good’ (read relatively ‘safe’) investments to grow it. The overt and stealth creation of money at the Federal Reserve will continue to erode the purchasing power of all who depend upon the money to be there when it matters the most.

If we put all emotion aside for the moment we can see that the government, while seeing itself as separate from the people, will gladly point out that it is of and for the people. So whatever the 'collective' needs to sacrifice in order to keep it going is the right thing to do. There is logic to this viewpoint if one believes the alternative is chaos and anarchy and lives in fear of those scenarios. Many involved in public policy setting do not think people are capable of governing themselves, let alone protecting themselves. This now seems to include planning for their elder years, both how one might live as well as die.

So what is the alternative? How might we view our elderly future? What can be done?

With our eyes wide open, questioning everything is a good start. Rethinking our needs and wants, reevaluating our priorities, and assessing what we might really value versus what society has told us is important. These are no small tasks and indeed can be a most humbling process to consider, but the upside of doing so could make all the difference.

While Cog and I continue to question and rethink our plans, these are the ways we have gone about replacing the concept of retirement with a different type of perceived security.

1. Getting our money out of money has perhaps been the most difficult step to take. The world still operates with money and the US dollar still spends. Sure, things cost a bit more, but nothing has spun out of control on a day to day basis to change the function of money just yet. But because the US dollar ‘trigger event’ and its timing will remain unknown to us plebs until it unfolds, we are erring on the side of caution and assume there won't be time to re-jigger our finances then.

What does this mean? We begin by only keeping enough cash in the bank to cover bills and immediate shopping and spending needs. Savings accounts and money markets don't earn interest, so they were eliminated.

2. Minimizing our counter-party risk was similar to a Wild West shoot out. Everywhere we looked targets had to be taken out. The rules for musical chairs (Calvinball style) say that whoever doesn't possess a seat when the music stops loses. And furthermore the rules can be changed at any time. So as we looked at just where our assets were distributed it turned out that most, if not all, of them were dependent upon a third party (oftentimes several layers of third parties) to do (or be) something in order to return the value of our investment to us.

Most obvious to us were brokerage accounts and safety deposit boxes that we closed out. Eliminating counter-party risk involves taking possession of any assets and items that will store earnings and wealth. Taking possession of precious metals, aka stacking gold and silver, is the most common way discussed. More contrarian ‘experts’ are now coming forth to say farm land, useful tools and investing in the knowledge of an valuable trade or skill are some of the best assets one can possess, none of which depends upon another party.

3. Arranging not to be at the mercy of rising interest rates is a key element to forwarding our plan for independence. This means getting rid of any debt which may be subject to rate increases. Ben Bernanke may have stated that interest rates will not rise in his lifetime, but he has been mistaken and/or disingenuous in the past. I cannot adequately express the personal relief it has brought us to not be subject to credit card interest or the worry about resets on mortgages with an ARM in five years.

When the day finally arrives when interest rates begin to raise substantially, certain costs will go up in tandem. Government entities on the Federal, State and local levels will get socked with rising interest payments payable on new or reissued bonds, and all taxes will rise accordingly. The same is true of corporations that depend upon debt issuance such as utilities. Supplying ourselves with alternatives at today's prices may be a bargain in hindsight.

4. Creating streams of income not reliant on a collapsing job market or an employer with constraints is providing us continuity in a rapidly changing landscape. Charles Hugh-Smith has recently written about the emergence of a new type of entrepreneur he has labeled Mobile Creatives. http://www.zerohedge.com/news/2014-05-01/meet-new-labor-class-mobile-creatives That article is a fascinating analysis of an emerging class of workers; this idea seeks to eliminate income dependency upon the state and corporations.

5. More self sufficient living arrangements was an essential step in preparing for our second half of life from several aspects. We collapsed previously diversified ‘retirement’ funds into a home with some land that has no debt as well as resources and tools that supply us with the ability to feed ourselves. By doing so, we now enjoy a much healthier lifestyle while converting our ‘money’ into tangible assets that will retain value for us.

6. We have taken charge of our health (care) because the current system is so dysfunctional and the previous methods for doing so (a good health insurance plan and reliable medical care) are now largely obsolete. Cog and I have made the decision to take complete responsibility for our own wellness. What this translates into is no dependency upon prescription or regular over the counter medicines. Nature provides far more potent remedies including powerful antibiotics and anti-cancer substances. We have elected to maintain our high deductible ‘health insurance’ policies in case the need for emergency medical treatment arises. Most important we do not mentally or emotionally rely on the members of the medical profession to keep us well or ‘heal’ sickness. I personally feel this has been the most empowering of all the steps we have taken to become more self-reliant.

Without question there are things we cannot provide for ourselves. No man is an island. As we get older, we recognize that we may need help with things and act accordingly by trying to assist others in the spirit of the Golden Rule.

There is little doubt that the years ahead bring promises of drastic and unknown changes. By addressing our future years and making changes while we are able, we are both less dependent upon our community and have an increased ability to contribute. It is never too late to reevaluate the way we take responsibility for ourselves.

Hello, Mrs. Cog:

I have to say – you did a bang-up job on this one. I followed it over at ZeroHedge.com as the comment thread grew and was delighted to see how elegantly both of you juggled all of the varied input. Well done and VERY well written!

Now, I hope some of them come on over here to see what you two are doing with TIF. I think a lot of the readers there would find the content here both intriguing and, frankly, refreshing (like a cold bucket of water over their heads) after all the ‘sturm und drang’ of the sweaty ZH environs. :)

Moar, please, Mrs. Cog! ZH needs your well-thought-through ‘seasoning’ on occasion – as do we denizens of TIF.

Much Appreciated,

L/L

This is why I subscribe. Well written. I inform myself with what’s going on in the world and then look for folks who are making the change also. I listen and learn from them.

I have already done some of the things on your list. We are in the middle of paying thru the nose for cashing in a 401k but it had to be done. We reinvested it in a rental house but don’t know how long we will keep it. I am developing some springs on our farm to provide water for domestic use (and maybe provide some electricity). My knowledge of beekeeping, queen rearing, and marketing honey may be important one day. Since I don’t have a farm to take care of while I’m in China I have been educating myself by watching Engineer 775 on youtube. Tools are an investment.

While we are in China my inner gardener lives vicariously thru you and Cog. Can’t wait to see the harvest pics.

good afternoon, mrs.cog ….

i read this article on “rethinking the concept of retirement” with interest (pun intended) … i certainly realize that it makes sense for those people who have savings accounts, and/or investments, and/or 401k’s, and/or mortgages, and/or credit card debt, and/or stocks ‘n’ bonds, etc.

but what about the person with none of the above?

my sister and i, she is 54 and i am almost 62, were having some fun awhile back discussing our “golden years” …

neither of us have any of the above … we were raised rich and by that i mean that our family was upwardly mobile: we were educated in private schools, belonged to country clubs, lived in big houses on acres of land, and daddy had the newest lincoln continental every year, as well as a jaguar xke, and a motorhome and a station wagon for mother, etc etc

as girls, we were raised well and sent to boarding school where it was assumed we would meet the right kind of people, make connections for later in life and ultimately … to marry well …

it didn’t quite go as our parents planned, though (*smiling*) and here was the BEST idea we hatched: (1) research the women’s prisons in all states, find the newest one which offers the best activities (2) go to that state and commit a victimless crime (we would never hurt anyone) (3) turn ourselves in for aforementioned crime (we never determined exactly what the crime would be) (4) voila! meals, roof over our head(s), medical care, uniform, plenty of time to read/write/use the library …

okay, so we did not intend to follow through, but i must say, in today’s crazy, upside-down, inside-out world, it did make some kind of sense at the time ….

and on the serious side, i have been taking your “take charge of health care” advice for decades … as well as simplifying life and self-sufficiency ideas … and here i am, feeling sort of smug with one of my mantras by way of bob dylan who sang: “when you ain’t got nuthin’, you got nuthin’ to lose”